In short, there was limited progress on updated targets and no major commitments from the outgoing US administration, and also China remained silent.

Photo credit: DPAM

Insights by Gerrit Dubois, Responsible Investment Specialist DPAM

Progress was however made on the Carbon Market mechanism, with Article 6 finalised, allowing trade among broader market actors. Finally financing pledges only marginally improved, reaching USD 300 billion by 2035, far from the USD 1.3 trillion requested (and needed).

We need to step up the gas, figuratively speaking please!

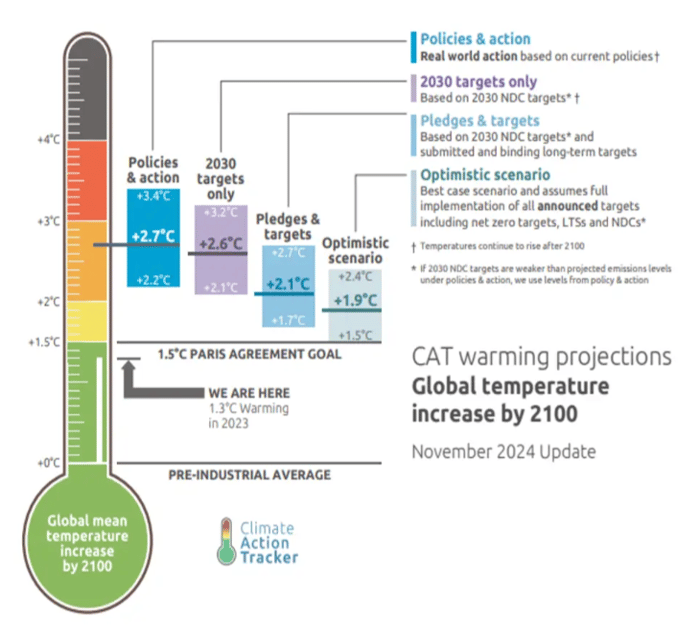

Welcome to COP29, the world’s largest gathering of backtracking and false promises! Although we’re already at the 29th edition, CAT research published this month shows that with current policies and actions, the world is on track for 2.7°C of global warming. Emissions need to decrease, so ambitions need to increase. And even though some claim the 1.5°C goal is dead, we should at least continue full throttle to limit the overshoot. Hence, we need to aim higher (with reductions) to finally land lower (in terms of global warming). A hopeful message comes from nations like Brazil (as a G20 country, not unimportant) and the UK, who revised their Nationally Determined Contribution (NDCs) in the first week. But we’ll have to wait for COP30 in Brazil, when nations will be required to submit revised (stronger) NDCs. We also need to stop talking about the cost of the transition and instead focus on the cost of inaction. This brings us to another major discussion point: financing.

Warming Projections - Global Temperature Increase by 2100

COP 29, the financing COP

COP29 in Baku is considered the ‘financing COP.’ But we all know the drill by now: the most difficult debates remain unresolved, either until the next COP or until the final days of the conference, resulting in a watered-down decision. This year was no different.

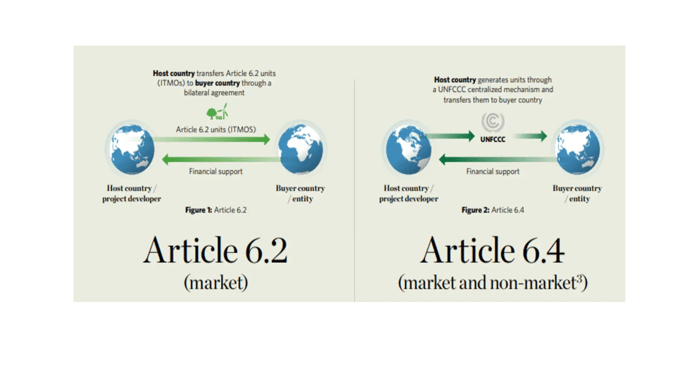

Climate finance, alongside mitigation, adaptation, and engagement, is a key obligation within the formal text of the Paris Agreement. What was at stake during COP29? Two main concepts: first, finalising the international carbon pricing mechanism, and second, new, improved financing solutions for developing countries, the so-called New Collective Quantified Goal (NCQG). The former, known as ‘Article 6,’ has already led to endless negotiations, although this time, prior to the start, two UN standards were finalised to facilitate market developments and ensure their associated credibility. As such, (private and public) projects generating credits will require approval from the host country and the UN Supervisory Body before credits can be issued. While bilateral trade will be allowed under Article 6.2 rules (through the use of ‘internationally transferred mitigation outcomes’ or ITMOs), and the finalised Article 4.2 will now allow broader market actors to engage in ITMO generation and trade.

Carbon Markets - how Article 6.2 and Article 6.4 will work

In terms of improved financing solutions for developing countries, it had already been agreed to revise up the USD 100 billion per year towards developing countries. However, this revision led to expected debate due to requests from high-income countries to revise the accounting structure, while at the same time addressing the balance between loans and grants. The total amount of financing will come from various sources, beyond loans and grants, such as carbon markets, voluntary contributions, multilateral development banks, and private finance, totaling a required USD 1.3 trillion per year by 2035 (as confirmed by leading climate economists). However, these solutions, and other offerings tied to standard interest rates, might lead to ‘sleight of hand accounting’ as the climate finance negotiator for the Alliance of Small Island States warned.

The final text, however, includes a voluntary commitment of USD 300 billion per year by 2035, from both public and private markets and led by developed markets.

Finally, the COP text also contains a provision for the establishment of a support program for the implementation of National Adaptation Plans (NAPs) for the least developed countries, as well as the launch of the Baku Adaptation Road Map. However, much work remains to be done in order to translate the National Adaptation Plans and all associated programs and roadmaps into tangible outcomes.

US and China, market giants remaining conspicuously silent in the debate

Finally, the new US administration puts the Paris Agreement at risk once again. Although it remains unclear to what extent key policies like the IRA might be repealed (as this could cost taxpayers a fortune, according to a recent publication by Johns Hopkins University), the America-first approach might make climate financing from the US to developing countries more difficult. Even Darren Woods, CEO of ExxonMobil has stated that withdrawal from the Paris Agreement is not ideal and that the continuation of Biden’s climate legislation should be upheld. There is also value in his statement about transition financing: ‘what the world needs is a transition that companies can make money in and generate returns on.’ It is unlikely that this includes accounting for historic (and current) externalities caused by products and services.

Alongside the US, China’s role also remains unclear. Although its per-capita emissions remain relatively low, its cumulative emissions since 1850 have now exceeded Europe’s emissions for the first time, raising questions about its desire to remain aligned with developing countries and avoid direct responsibility for climate finance. On the other hand, China seems determined to defend its leading position in the clean energy supply chain, ready to take on additional opportunities if the US backtracks.

Restatement, for what it’s worth?

The US and EU began the first week pushing for a finance deal, while restating the COP28 commitments to transition away from fossil fuels, triple renewable energy and double energy efficiency (note that progress was made on only one of the three). Although the emphasis was placed on the financing agreement, the restatement of initial commitments was pushed back on by some nations, including Saudi Arabia. As a result, the final text omitted strong references to last year’s landmark decision to ‘transition away from fossil fuels,’ with only indirect references remaining. On the positive side, some nations committed to phasing down fossil fuel subsidies by joining the coalition launched at COP28, while another delegation pledged to cease the construction of new unabated coal power plants.

COP30: let’s meet in a hotter, more dangerous world

Knowing the average global cost of climate-related damage amounted to USD 16 million per hour between 2000 and 2019, and 2024 was a record-breaking year in terms of emissions and climate change damages (with the US facing an astonishing USD 100 billion in the first half of the year), COP30 might be held in times of crisis where costs of climate change damages are continuing to soar. However, COP30 in Brazil will matter, a lot. The second round of NDCs is scheduled, while further implementation of the different financing streams will be assessed. Furthermore, trade tensions due to the new US administration might change the dynamics of global collaboration. COP30, brace for impact.

Disclaimer:

Marketing Communication. Investing incurs risks.

The views and opinions contained herein are those of the individuals to whom they are attributed and may not necessarily represent views expressed or reflected in other DPAM communications, strategies or funds.

The provided information herein must be considered as having a general nature and does not, under any circumstances, intend to be tailored to your personal situation. Its content does not represent investment advice, nor does it constitute an offer, solicitation, recommendation or invitation to buy, sell, subscribe to or execute any other transaction with financial instruments. Neither does this document constitute independent or objective investment research or financial analysis or other form of general recommendation on transaction in financial instruments as referred to under Article 2, 2°, 5 of the law of 25 October 2016 relating to the access to the provision of investment services and the status and supervision of portfolio management companies and investment advisors. The information herein should thus not be considered as independent or objective investment research.

Investing incurs risks. Past performances do not guarantee future results. All opinions and financial estimates are a reflection of the situation at issuance and are subject to amendments without notice. Changed market circumstance may render the opinions and statements incorrect.

Published by

investESG

investESG

investESG