What US–EU Divergence Means for Portfolio Performance

Photo credit: Nicholas Cappello / Unsplah+

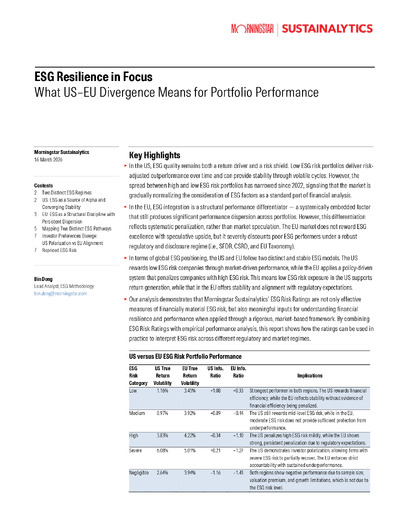

In the US, ESG quality remains both a return driver and a risk shield. Low ESG risk portfolios deliver riskadjusted outperformance over time and can provide stability through volatile cycles. However, the spread between high and low ESG risk portfolios has narrowed since 2022, signaling that the market is gradually normalizing the consideration of ESG factors as a standard part of financial analysis.

In the EU, ESG integration is a structural performance differentiator — a systemically embedded factor that still produces significant performance dispersion across portfolios. However, this differentiation reflects systematic penalization, rather than market speculation. The EU market does not reward ESG excellence with speculative upside, but it severely discounts poor ESG performers under a robust regulatory and disclosure regime (i.e., SFDR, CSRD, and EU Taxonomy).

Low ESG risk exposure in the US supports return generation, while that in the EU offers stability and alignment with regulatory expectations.

In terms of global ESG positioning, the US and EU follow two distinct and stable ESG models. The US rewards low ESG risk companies through market-driven performance, while the EU applies a policy-driven system that penalizes companies with high ESG risk. This means low ESG risk exposure in the US supports return generation, while that in the EU offers stability and alignment with regulatory expectations.

Our analysis demonstrates that Morningstar Sustainalytics’ ESG Risk Ratings are not only effective measures of financially material ESG risk, but also meaningful inputs for understanding financial resilience and performance when applied through a rigorous, market-based framework. By combining ESG Risk Ratings with empirical performance analysis, this report shows how the ratings can be used in practice to interpret ESG risk across different regulatory and market regimes.

Join the conversation

Go deeper into the data by attending our upcoming webinar, ESG Resilience in Focus: How Markets Price Risk and What It Means for Portfolios, with the analysts behind the research on May 28, 2026. We’ll explore:

- How U.S. and EU markets price sustainability risk differently, and what that signals for investors

- How investors can evaluate trade-offs between resilience, returns, and sustainability outcomes across regions

- How these pricing signals show up in portfolios, influencing benchmark design, portfolio construction, and durability across market cycles

Published by

Morningstar Sustainalytics